Selling National Firearms Act (NFA) items presents unique challenges that most retailers never encounter. While a standard firearm transaction can often be completed the same day, suppressors, short-barreled rifles, short-barreled shotguns, and other regulated items may involve approval timelines measured in months rather than minutes.

These extended timelines create operational, financial, and customer-service challenges that require careful planning. Payment collection, inventory management, customer communication, and recordkeeping all become significantly more important when transactions remain open for extended periods.

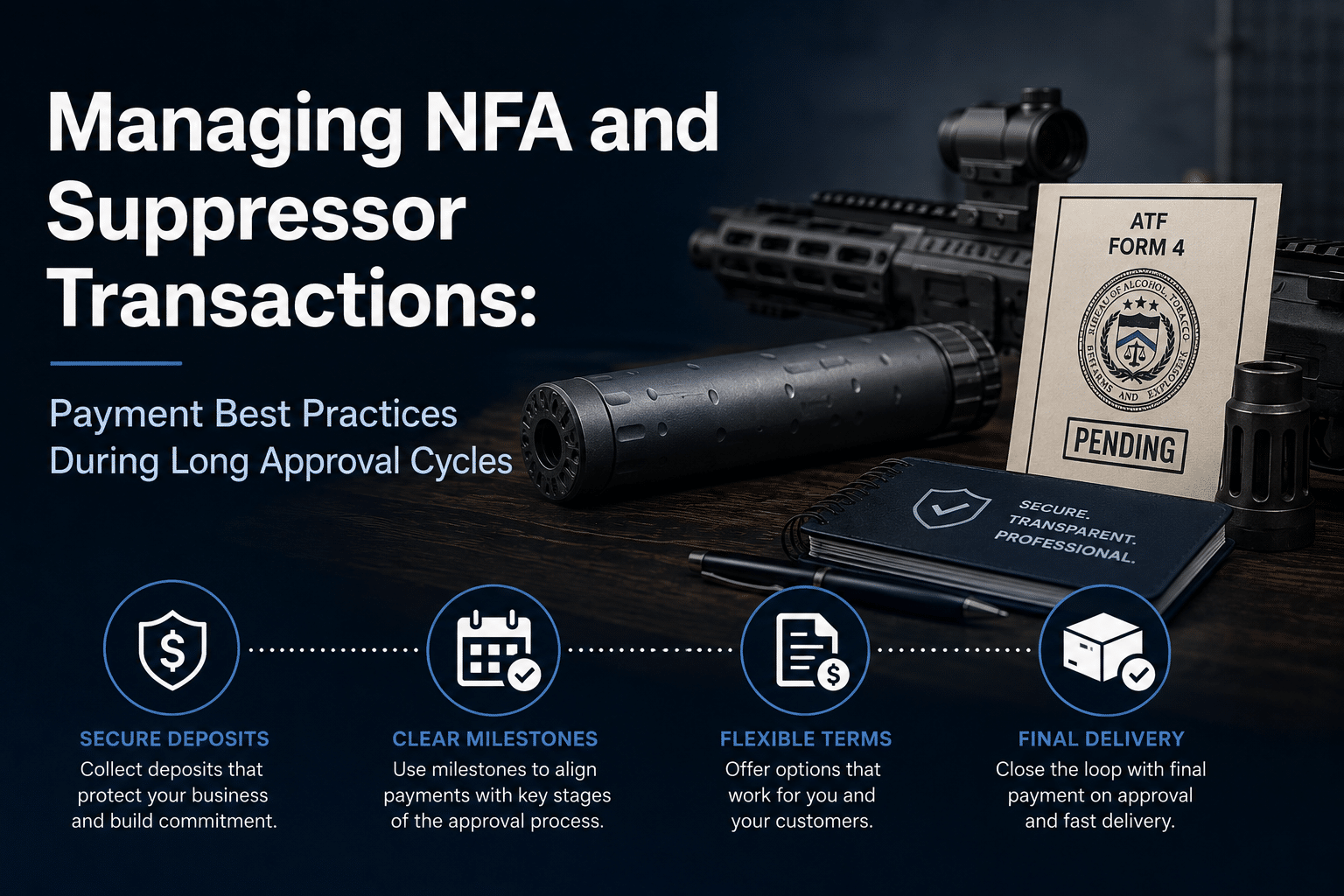

For dealers who regularly sell suppressors and other NFA-regulated products, establishing clear payment procedures can improve cash flow, reduce customer frustration, and minimize disputes.

Why NFA Transactions Are Different

Most retail purchases follow a predictable pattern.

A customer selects a product, completes payment, takes possession, and the transaction concludes.

NFA transactions are fundamentally different.

Customers often commit thousands of dollars to a purchase they may not physically receive for many months. During that waiting period, questions arise regarding payment timing, refunds, cancellations, storage, and communication.

Without clearly defined policies, misunderstandings can develop quickly.

Customers may forget details discussed during the original purchase. Staff turnover may occur. Regulatory timelines may shift. Market conditions may change.

A structured payment process helps ensure everyone remains aligned throughout the transaction lifecycle.

Choosing the Right Payment Structure

There is no universal payment model that works for every dealer.

However, most successful NFA retailers utilize one of three approaches.

Full Payment Up Front

Some dealers collect the entire purchase amount at the time of sale.

This approach offers several advantages:

- Immediate cash flow

- Simplified accounting

- Reduced collection risk

- Clear inventory commitment

For high-demand suppressors and specialty items, full payment often makes sense because inventory is effectively reserved for a specific customer.

The downside is that some customers may hesitate to pay in full for an item they cannot immediately take home.

Deposit Plus Final Payment

Another common approach involves collecting a substantial deposit initially and the remaining balance later.

This structure can make larger purchases more accessible while still protecting the business.

Deposits help cover:

- Inventory acquisition costs

- Administrative expenses

- Processing fees

- Opportunity costs associated with reserving inventory

Customers often appreciate the flexibility while retailers maintain a level of financial protection.

Payment Plans

Some dealers offer structured installment arrangements during the approval period.

Because approval timelines may extend for several months, the waiting period naturally creates an opportunity for scheduled payments.

Payment plans can help customers budget for larger purchases while creating recurring revenue opportunities for the business.

However, dealers should ensure policies are clearly documented and consistently administered.

Establishing Clear Deposit Policies

If deposits are used, customers should fully understand the terms before making a commitment.

Questions that should be addressed include:

- How much is required upfront?

- Is the deposit refundable?

- What happens if the customer cancels?

- What happens if the product becomes unavailable?

- How are processing fees handled?

Clarity is critical.

Many customer disputes stem from assumptions rather than actual disagreements.

Providing written policies at the time of sale helps prevent misunderstandings later.

Managing Customer Expectations

One of the biggest challenges in NFA retail is expectation management.

Customers are often excited when they place an order. That enthusiasm can turn into frustration if communication disappears during the approval process.

Dealers should explain:

- Expected timelines

- Potential delays

- Approval uncertainties

- Required documentation

- Next steps after approval

Customers who understand the process generally have a better experience than those left guessing.

Even when timelines change, informed customers tend to be more patient and cooperative.

Communication During the Waiting Period

Regular communication can dramatically improve customer satisfaction.

Many retailers focus heavily on the initial sale and final delivery while neglecting the months in between.

Simple updates can help customers remain engaged and confident.

Useful communication opportunities include:

Order Confirmation

Immediately confirm:

- Product details

- Payment received

- Documentation submitted

- Expected next steps

Status Updates

Periodic updates reassure customers that their transaction remains active.

Even when there is no significant news, a brief check-in can reduce anxiety.

Approval Notification

When approval arrives, customers should be contacted promptly and provided with clear instructions regarding pickup procedures and any remaining balance.

Inventory Management Considerations

Long approval periods create inventory management challenges.

Items may remain allocated to a customer for months.

Retailers should establish procedures regarding:

- Reserved inventory

- Special orders

- Storage requirements

- Transfer documentation

- Inventory reconciliation

Accurate records become increasingly important as transaction timelines expand.

Mistakes that might be corrected quickly in standard retail environments can become far more complicated during lengthy NFA transactions.

Avoiding Chargebacks and Disputes

Although NFA customers are often highly committed buyers, disputes can still occur.

Common causes include:

- Misunderstood timelines

- Poor communication

- Unexpected delays

- Confusion regarding refunds

- Billing misunderstandings

Several best practices can help reduce risk.

Use Detailed Receipts

Transaction records should clearly identify:

- Product descriptions

- Deposit amounts

- Remaining balances

- Terms and conditions

Maintain Signed Documentation

Whenever possible, customers should acknowledge relevant policies before payment is processed.

Document Communications

Email confirmations and written updates provide valuable records if questions arise later.

Be Transparent

Customers are generally more understanding when they receive timely and accurate information.

Handling Cancellations

Cancellation requests occasionally occur despite best efforts.

A customer may experience financial difficulties, relocate, or simply change their mind.

Businesses should establish cancellation policies before these situations arise.

Policies may address:

- Refund eligibility

- Special-order inventory

- Administrative expenses

- Restocking considerations

- Payment processing costs

Consistency is essential.

Applying policies uniformly helps reduce complaints and protects the business from accusations of unfair treatment.

The Importance of Secure Payment Systems

Because NFA transactions often involve higher ticket values, payment security becomes especially important.

Customers expect their financial information to be protected throughout the transaction lifecycle.

Modern payment systems can help dealers provide:

- Secure card storage

- Tokenized payment profiles

- Digital invoicing

- Electronic receipts

- Online payment options

These capabilities improve convenience while reducing security risks associated with manual payment handling.

Supporting Long-Term Customer Relationships

NFA customers frequently become repeat customers.

A positive suppressor purchase experience may lead to future purchases involving firearms, accessories, optics, memberships, training programs, or additional regulated items.

This makes customer experience particularly important.

Retailers who communicate effectively, maintain organized records, and provide a transparent payment process often earn long-term loyalty.

The waiting period can either strengthen or weaken customer relationships depending on how the business manages expectations.

Creating a Better NFA Transaction Experience

NFA sales are unlike almost any other retail transaction. The combination of regulatory requirements, extended approval timelines, and higher-value purchases creates unique operational challenges.

Dealers who rely on informal processes often encounter avoidable issues related to communication, cash flow, and customer satisfaction.

By implementing structured payment procedures, clear policies, consistent communication, and secure payment technology, businesses can create a smoother experience for both customers and staff.

The goal is not simply completing a sale. It is maintaining confidence throughout a transaction that may remain active for many months. Dealers who accomplish that consistently are often rewarded with stronger customer relationships, fewer disputes, and increased long-term growth.