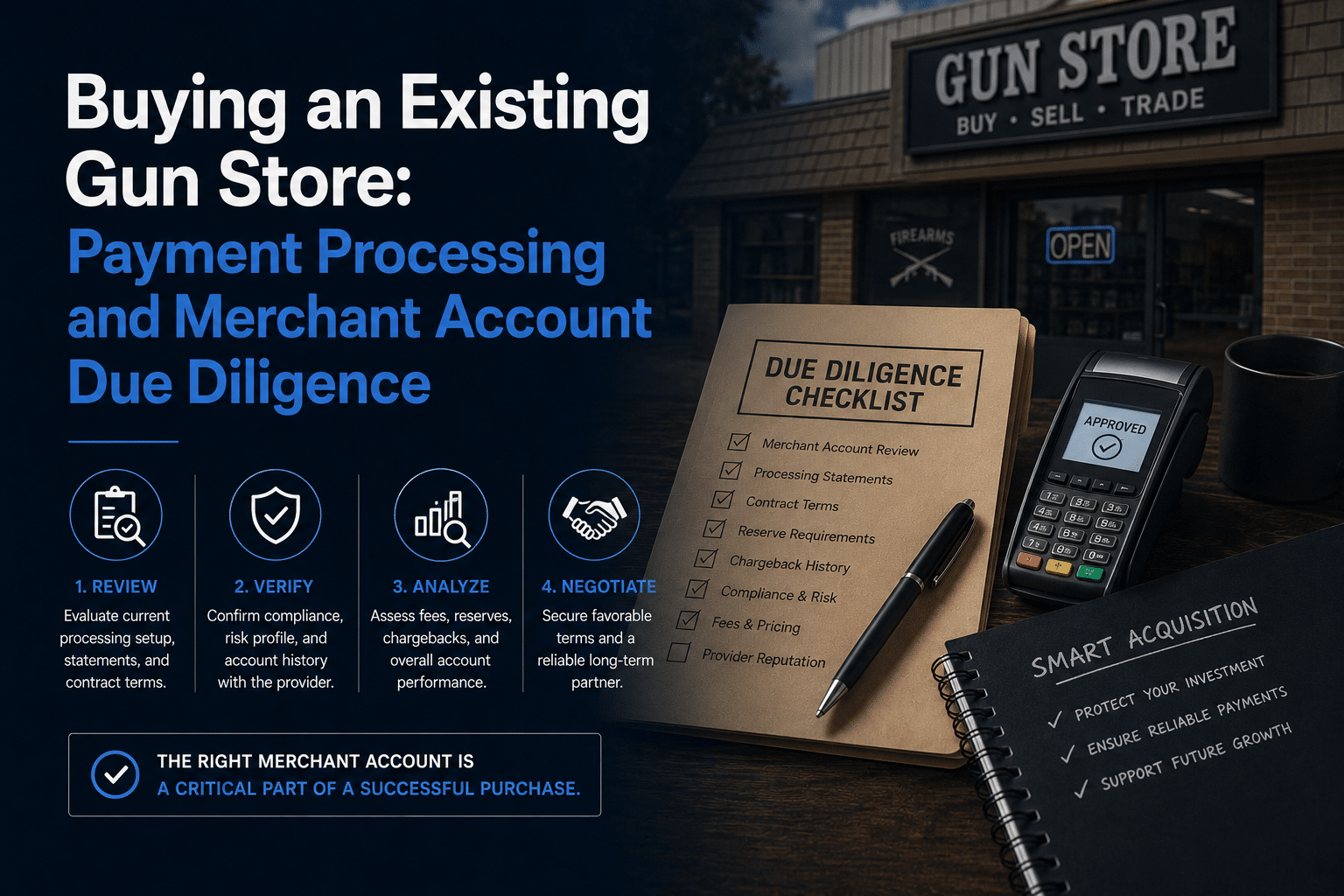

Purchasing an existing gun store can offer significant advantages compared to starting a business from scratch. Existing inventory, an established customer base, supplier relationships, trained employees, and operational systems can accelerate growth and reduce startup challenges.

However, many buyers focus heavily on inventory valuation, real estate, and licensing requirements while overlooking one of the most important operational components of the business: payment processing.

A gun store’s payment infrastructure affects everything from cash flow and profitability to customer experience and operational continuity. Failing to evaluate merchant services during due diligence can result in unexpected costs, processing interruptions, or expensive migration projects after the acquisition closes.

Before purchasing an existing firearms business, prospective buyers should carefully assess the payment systems that support daily operations.

Why Payment Processing Matters During an Acquisition

For most firearm retailers, payment acceptance is a mission-critical function.

Without reliable payment processing, sales stop.

While inventory, licenses, and physical assets are highly visible during an acquisition, payment infrastructure often operates in the background. Because it functions smoothly on a daily basis, buyers may underestimate its importance.

Yet the merchant account, gateway, point-of-sale integrations, ecommerce connections, and reporting systems often represent years of operational development.

Understanding how these systems work before closing can prevent major surprises later.

Start With the Merchant Account

One of the first questions buyers often ask is whether the existing merchant account can transfer to the new ownership entity.

In most cases, the answer is no.

Merchant accounts are typically underwritten based on a specific legal entity, ownership structure, and risk profile. When ownership changes, processors generally require a new underwriting process rather than simply transferring the account.

This is particularly important in the firearms industry, where underwriting standards are often more rigorous than those found in traditional retail sectors.

Buyers should discuss transition requirements early with their payment provider to avoid disruption.

Understanding Current Processing Costs

Many store owners know roughly what they pay for processing but may not fully understand how pricing is structured.

During due diligence, buyers should review several months of merchant statements.

Key areas to evaluate include:

Effective Processing Rate

What percentage of revenue is ultimately paid in processing fees?

Monthly Fees

Are there recurring charges for software, reporting, compliance programs, or equipment?

Gateway Fees

Are ecommerce gateways billed separately?

Additional Assessments

Are there fees for chargebacks, batch processing, PCI compliance, or support services?

Understanding the complete cost structure provides a clearer picture of operating expenses.

Reviewing Chargeback History

Chargebacks are an important indicator of operational health.

A business with excessive disputes may be experiencing issues related to customer service, documentation, fraud prevention, or transaction management.

Buyers should request information regarding:

- Historical chargeback volume

- Chargeback ratios

- Common dispute reasons

- Resolution processes

- Documentation practices

Strong dispute management procedures often indicate disciplined operations.

Conversely, poor recordkeeping may create unnecessary risk.

Evaluating Ecommerce Infrastructure

Many modern gun stores generate revenue through both physical and online sales channels.

As part of due diligence, buyers should examine how ecommerce transactions are processed.

Questions worth asking include:

- Which shopping cart platform is being used?

- What payment gateway is integrated?

- Are there custom integrations?

- How are online orders managed?

- How are transfers coordinated?

The complexity of ecommerce infrastructure varies significantly between businesses.

Understanding these systems before acquisition can help avoid unexpected transition challenges.

Point-of-Sale System Assessment

The point-of-sale system often serves as the operational hub of the business.

It may manage:

- Inventory

- Customer information

- Reporting

- Sales transactions

- Employee permissions

- Ecommerce synchronization

Changing ownership does not automatically eliminate these requirements.

Buyers should determine:

System Ownership

Is the software owned, leased, or subscription-based?

Integration Dependencies

What systems rely on the POS platform?

Contract Commitments

Are there long-term agreements in place?

Data Portability

Can transaction and customer records be exported if necessary?

Understanding these factors helps support a smoother transition.

Identifying Contractual Obligations

Many payment service agreements contain provisions that may affect an acquisition.

These can include:

- Equipment leases

- Service agreements

- Software subscriptions

- Gateway contracts

- Support arrangements

Buyers should review these obligations carefully.

An attractive purchase price can quickly become less attractive if substantial contractual liabilities are discovered after closing.

Assessing Equipment and Hardware

Physical payment hardware should also be reviewed.

Evaluate:

- Terminal age

- Device condition

- Contactless payment support

- Integration capabilities

- Warranty status

Older equipment may continue functioning adequately, but replacement costs should be factored into acquisition planning.

Many retailers use this opportunity to modernize systems as part of broader operational improvements.

Customer Experience Considerations

Payment infrastructure directly affects customer experience.

During due diligence, observe:

- Checkout speed

- Receipt delivery

- Mobile payment acceptance

- Contactless payment options

- Ecommerce checkout functionality

Customers increasingly expect convenience and flexibility.

If systems appear outdated or cumbersome, upgrades may become part of the post-acquisition strategy.

Planning the Transition

One of the most overlooked aspects of acquisitions is transition planning.

Even when new merchant accounts and systems are required, the goal should be minimizing disruption.

Key planning areas include:

Application Timing

Begin underwriting and account setup as early as possible.

Staff Training

Employees should understand new systems before launch.

Testing

Verify all integrations before switching over.

Customer Communication

If changes affect customer experience, proactive communication may be appropriate.

Successful transitions rarely happen by accident. They are the result of preparation.

Cash Flow During Ownership Changes

Business acquisitions can create temporary cash flow uncertainty.

Funding schedules may change as new merchant accounts are established.

Buyers should understand:

- Settlement timelines

- Reserve requirements

- Funding expectations

- Reporting access

Having adequate working capital available during the transition can reduce stress and improve operational flexibility.

Compliance and Documentation

Firearms businesses operate within a highly regulated environment.

Although payment processing and regulatory compliance are separate functions, documentation standards matter in both areas.

Strong businesses typically maintain organized records regarding:

- Transactions

- Refunds

- Chargebacks

- Customer communications

- System access controls

Well-documented operations generally create smoother ownership transitions.

Opportunities for Improvement

An acquisition can also provide an opportunity to improve payment operations.

Potential enhancements may include:

- Upgrading terminals

- Modernizing ecommerce systems

- Streamlining reporting

- Improving fraud controls

- Reducing processing costs

- Expanding payment options

The objective is not necessarily changing everything immediately.

Instead, buyers should identify opportunities that support long-term business goals.

Looking Beyond the Purchase Price

When evaluating a gun store acquisition, it is easy to focus on inventory, facilities, and revenue figures. While these factors are important, payment processing infrastructure deserves equal attention.

Merchant accounts, gateways, point-of-sale systems, chargeback management practices, and customer payment experiences all contribute to the overall health of the business.

A thorough review during due diligence can uncover risks, identify opportunities, and help ensure a smoother transition after closing.

For buyers entering the firearms industry, understanding the payment ecosystem is not simply an operational exercise. It is an essential part of protecting the investment and positioning the business for future growth.